CPSI NewsWire brings you market updates on Mongolia, compiled by CPS International, a Mongolian marketing arm of CPS Securities, a Perth, WA based stockbroking and corporate advisory firm, specialising in capital raising for mining and junior stocks. Follow CPSI NewsWire on Twitter, Facebook

Mongolia Delays $3 Billion Coal IPO to Retain Hong Kong Plan

March 7 (Bloomberg) Erdenes Tavan Tolgoi, the Mongolian coal miner planning a $3 billion initial public offering, said it delayed the foreign part of the deal by at least two months to September to help win listings in London and Hong Kong.

The state-run miner may list locally first as part of the government program to give citizens stock in the company and then pursue a sale overseas, Chief Executive Officer Baasangombo Enebish said today in an interview in the nation’s capital, Ulan Bator. Prime Minister Sukhbataar Batbold’s government had aimed to complete the IPO before June elections.

Mining companies have lost 27 percent of their market value since April last year, the Bloomberg World Mining Index shows, as global economic volatility curbed demand for resources. The IPO will mark Mongolia’s first listing of a state-run miner overseas as the country seeks to use its mineral riches to support an economy that grew by a record 17.3 percent last year.

“Ideally, we’d like to go to Hong Kong and London together,” Enebish said, adding that Hong Kong law currently restricts accepting Mongolia as a jurisdiction for listed companies. “And first we need to clarify what percentage we can actually sell in the IPO.”

Mongolia’s parliament is due to vote on a new securities law that should allow entities registered in the country to be accepted by the Hong Kong stock exchange, Enebish said. Erdenes TT, as the company is known, would list shares or depositary receipts in Hong Kong. The London listing would be of global depositary receipts, he said.

Goldman Sachs

Goldman Sachs Group Inc., Deutsche Bank AG, BNP Paribas SA and Macquarie Group Ltd. have been hired as financial advisers, Otgonbat Sedbazar, an adviser to the nation’s Resources Ministry, said in November.

Erdenes TT is developing the East Tsankhi part of the 6 billion-metric-ton Tavan Tolgoi coal deposit, one of the world’s biggest untapped sources of the fuel until mining began last year. The IPO may raise more than $3 billion, Mongolian cabinet office chief Khurelbaatar Chimed said in September.

The Mongolian government has pledged to distribute as much as 20 percent of the Erdenes TT shares to citizens as a way of fulfilling past election promises of spreading the country’s growing wealth. A third of Mongolians live below the poverty line, according to the World Bank.

Rail, Power

The coal company is also considering a sale of convertible bonds before listing, Mongolia’s Minerals and Energy Minister Dashdorj Zorigt said in a March 5 interview. The government won’t press Erdenes TT to complete the IPO before a parliamentary election in June, allowing the timing and place of sale to be decided on a “commercial” basis, he said.

Erdenes TT is due to start rail, road and power generation facility construction this spring and summer which will help to expand output, Enebish said. Delaying the international share sale will help the company “add in value,” he said.

Erdenes TT produced almost 1 million tons of coal last year and targets 3 million tons this year. The company is due to build a coal-washing facility this year so that it can offer higher-value products.

The state-owned miner also owns the license to the West Tsankhi coal area next to its operating site. Mongolia last year started a tender with foreign companies including Peabody Energy Corp. (BTU) to offer the rights to develop that deposit. The winners would pay Erdenes TT royalty fees.

A “clarification” of the situation around the tender will also help Erdenes TT’s IPO, Enebish said, saying that the process is being managed by the Mongolian government.

Related:

Huge Mongolian mining float delayed – Financial Times, March 8

Mongolia’s Tavan Tolgoi Coal Stalled as Politics Overtake Mining

March 8 (Bloomberg) Mongolia’s plans to develop part of the Tavan Tolgoi coal deposit, one of the world’s largest sources of the fuel, have stalled amid political jousting ahead of June parliamentary elections.

Progress on talks with companies including Peabody Energy Corp. (BTU), OAO Russian Railways (RZHD), and China’s Shenhua Group to develop the West Tsankhi part of Tavan Tolgoi have “stopped,” Prime Minister Sukhbaatar Batbold said. The $3 billion initial public offering of state-run Erdenes Tavan Tolgoi, which is developing the East Tsankhi part of the 6-billion-metric-ton field, was delayed yesterday as some politicians call for Mongolia to develop West Tsankhi itself.

“This is a democracy and there should be different opinions,” Batbold said in an interview in Ulan Bator, Mongolia’s capital, without saying which he supported. He backed Rio Tinto Group (RIO) last year against a group of 20 lawmakers who demanded that Mongolia get a bigger stake in the company’s Oyu Tolgoi copper project.

Batbold’s push to lure investors and modernize an economy that grew 17.3 percent in 2011 is being stymied as election campaigning unfolds. The Mongolian Democratic Party left Batbold’s coalition government in January and President Tsakhia Elbegdorj, formerly a member of the MDP, told an economic forum in Ulan Bator this week that the country has shown “no execution, no performance” since 2010.

“There is some election campaign posturing ahead of June,” said Randolph Koppa, chief executive officer of Trade and Development Bank, based in Ulan Bator.

Mitsui, Itochu

Batbold travels this week to Japan, which has several companies involved in the West Tsankhi bidding. Mitsui & Co. partnered with Shenhua in the bid and will persevere with it, head of resources Fuminobu Kawashima said earlier this month. Rival Japanese trading companies including Itochu Corp. (8001) are bidding with South Korean and Russian companies.

Mongolia first announced and then said it would review an accord in July that planned to give Shenhua Group a 40 percent stake in West Tsankhi, with Peabody taking 24 percent and a Russia-Mongolian group the rest. The government didn’t clarify who the Russia-Mongolia group included.

While the future of the West Tsankhi project remains in doubt the $3 billion initial public offering of Erdenes TT, as the company is also known, will be delayed since the state-run miner is the license holder for the area and would receive royalty fees from the ultimate bid winner.

Cash Handout

Erdenes TT also needs parliament to pass a new law to allow it to list shares in Hong Kong and determine what part of its equity will be distributed to the public, Chief Executive Officer Baasangombo Enebish said March 7 in an interview.

Batbold’s Mongolian People’s Party promised 1 million tugrik ($750) in cash to all adults among Mongolia’s 3.1 million people before the last election. The party must keep its promise and that can be done with cash or Erdenes TT shares, Batbold said. Legislation on this and on securities is being reviewed by parliament, he said.

It isn’t clear when legislation will pass or be adopted, Batbold said in his office at the state palace, where he presided over the annual Mongolia Economic Forum. He said he couldn’t give a time frame for the IPO of Erdenes TT.

Before Batbold came on-stage for the forum’s closing remarks on March 6, Elbegdorj made an unscheduled appearance. In his speech, Elbegdorj said that he didn’t take part in the annual forum this year because the government had talked much and delivered little.

Electoral Limitations

“We have limitations in our four-year electoral cycle,” Elbegdorj said. “Only one year of four is productive and half of that is winter,” he said.

Government staff has bloated by 50 percent in the past two years and the state’s involvement in the economy is too great, Elbegdorj said. Politicking and corruption have slowed the country’s major projects while the government has placed too much emphasis on mining, he said.

Current lawmakers should “rest peacefully and walk away” after the next election, Elbegdorj said. The next presidential election is scheduled for 2013.

The political tensions come as Mongolia’s economy enters a “red light” zone, according to Paul Holden, director of the Gunnison, Colorado-based Enterprise Research Institute. Bank lending rose 70 percent last year and money supply increased by 40 percent, Holden said on the sidelines of the Mongolia forum.

Risks Compounding

“Risks are compounding,” Holden said.

State spending doubled in the past two years in real terms with retail trade becoming the major driver of Mongolia’s record economic expansion last year, the World Bank said in a report last month. The country’s mining industry grew 8.7 percent last year to the economy’s 17.3 percent, the bank said.

State cash flows accounted for about half the country’s 11 percent inflation, last year, Naidansuren Zoljargal, a deputy governor at the Bank of Mongolia, told the economic forum. Spending has been driven by the politicians’ short-term election campaigning, hurting private-sector profit margins, and leaving the central bank to “clean up the mess,” he said.

Batbold denied that the government has stopped functioning ahead of elections, saying construction of major road and rail infrastructure will commence this year now that a study into the Tavan Tolgoi coal transport railroads has been completed.

Both East and West Tsankhi need rail links to boost output and cut costs. Mongolia is planning a $5.2 billion development that involves a route northeast to Russia and south to China.

Mongolia will pursue both routes simultaneously, Batbold said. How this will be financed is also becoming more clear, with the state-owned Development Bank of Mongolia LLC and “other institutions” working together, Batbold said.

The Development Bank of Mongolia will today start marketing dollar-denominated bonds as part of a $600 million Euro Mid Term Note program with ING Groep NV. (INGA)

“Not everything is about the election,” Batbold said. “Government has to work constantly.”

975 trading +2.57% to HK$7.98 at time of writing

MMC enters into US$300M loan facility with a commercial bank

March 9, Mongolian Mining Corporation (HK:975) --

Pursuant to the requirements under Rule 13.18 of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Listing Rules”), the board of directors (the “Board”) of Mongolian Mining Corporation (the “Company”) announces that on 8 March 2012, the Company as a borrower entered into a facilities agreement (the “Facilities Agreement”) with a commercial bank as original lender (the “Bank”). The Facilities Agreement relates to the provision of term loan facilities of up to US$300,000,000 (the “Facilities”) to the Company. The Facilities shall be repaid by the Company in installments with the last repayment date falling 36 months after the date on which the first loan under the Facilities is made. Thus the Facilities with 3 year tenor will allow the Company to partially refinance its existing loan and extend maturity of funding facilities.

Under the Facilities Agreement, it will be an event of default if, among other things, MCS Holding LLC (“MCS”), an indirect controlling shareholder of the Company, ceases to beneficially hold (directly or indirectly) at least 30 per cent. of the issued share capital of the Company from time to time without the prior written consent of all lenders under the Facilities Agreement. If the above event of default occurs, such lenders may, by notice to the Company: (a) cancel the total commitments at which time they shall immediately be cancelled; (b) declare that all or part of the loans, together with the accrued interest, and all other amounts accrued or outstanding under the finance documents be immediately due and payable to the lenders, at which time they shall become immediately due and payable; (c) declare that all or part of the loans be payable on demand, at which time they shall immediately become payable on demand; and (d) direct the security agent to exercise any or all of its rights, remedies, powers or discretions under the finance documents.

The Company will include appropriate disclosure in its interim and annual reports for so long as circumstances giving rise to the disclosure obligation under Rule 13.18 of the Listing Rules continues to exist.

MMC Annual Report 2011

March 6, Mongolian Mining Corporation (HK:975) --

HIGHLIGHTS

In 2011, the Group has successfully completed all major production and infrastructure development projects in line with its strategic objectives, resulting in the Company’s transformation into a fully-fledged coal mining, processing, transportation, and marketing platform.

For the year ended 31 December 2011, the Group’s production of run-of-mine (“ROM”) coal reached approximately 7.1 million tonnes, surpassing the Group’s original target of 7.0 million tonnes by approximately 0.1 million tonnes and representing a year-on-year increase of approximately 82.1% (2010: 3.9 million tonnes).

The Group’s revenue amounted to approximately USD542.6 million for the year ended 31 December 2011, representing an increase of approximately USD265.1 million, or approximately 95.5% as compared to approximately USD277.5 million for the year ended 31 December 2010.

The profit attributable to the equity shareholders of the Company for the year ended 31 December 2011 was approximately USD119.1 million, representing an increase of approximately USD59.0 million, or approximately 98.2% as compared to approximately USD60.1 million for the year ended 31 December 2010.

Free cash flow generated from operations amounted to approximately USD21.0 million for the year ended 31 December 2011.

The basic earnings per share attributable to the equity shareholders of the Company amounted to approximately USD3.21 cents for the year ended 31 December 2011, as compared to approximately USD1.91 cents for the year ended 31 December 2010. The diluted basic earnings per share attributable to the equity shareholders of the Company amounted to approximately USD3.07 cents for the year ended 31 December 2011, as compared to approximately USD1.91 cents for the year ended 31 December 2010.

In view of the major production and infrastructure development projects committed or being planned by the Company, the Board decided not to pay any dividend for the year ended 31 December 2011 despite MMC’s record earnings (dividend in 2010: nil).

…

Announcement made after market close. PCY closed +5.43% to 48.5c

Prophecy Coal Closes $10 Million Private Placement

VANCOUVER, BRITISH COLUMBIA--(Marketwire - March 8, 2012) - Prophecy Coal Corp. ("Prophecy" or the "Company") (TSX:PCY)(OTCQX:PRPCF)(FRANKFURT:1P2) is pleased to announce the closing of the private placement previously announced on March 1, 2012. Due to investor demand, the Company has increased the size of the non-brokered private placement of common shares to 22,363,866 shares at a price of $0.45 per share for gross proceeds of $10,063,740 (the "Placement").

Company insiders invested $508,500 and together with existing shareholders have subscribed for a majority of this financing. Finder's fees of 6% of the proceeds placed, payable in cash, were paid on certain arms-length portions of the placement.

All shares issued are subject to a hold period expiring on July 9, 2012. Proceeds of the Placement will be applied to technical work at the Chandgana Thermal Coal Power Project, operations at the Ulaan Ovoo mine and general corporate purposes.

The Company also wishes to announce that it has granted options to acquire an aggregate of 3 million common shares at a price of $0.485 per share for a period of five years to directors, officers, consultants and employees of the Company. The above grant is subject to regulatory approval, including the approval of the TSX Exchange.

Ocean Equities Mongolia Exploration Update: Voyager Resources Ltd

March 9 (Ocean Equities) --

A maiden resource in the next quarter is expected to be a transitional point supporting an attractive mid-scale development project with further significant upside potential

Source of the Opportunity

Voyager Resources Ltd (‘Voyager’ or ‘the Company’) is the most advanced, independent copper exploration and development play in Mongolia with a controlling interest in three promising projects, all drill tested. Recent aggressive exploration at its flagship asset, the KM project (‘KM’), continues to intersect some of the best copper mineralisation reported in-country outside of the world-class Oyu Tolgoi (‘OT’) deposit with results highly encouraging from the three discoveries made since drilling commenced only 8 months ago. Encountered mineralisation has drawn comparisons to the Chilean porphyry systems and the project is located in the Edrene Island Arc Terrain which hosts a number of large mineralised porphyry systems including OT and the nearby Zuun Mod system.

The magmatic hydrothermal breccias intersected in drilling at the Cughur, Gaans (~2.5km to the east of Cughur) and, more recently, Aranjin prospects (~1km NE of Cughur) at the KM project are now believed to have formed as intrusive breccia pipes that have been emplaced or fed from a large porphyry stock or stocks. Five mineralised hydrothermal breccia pipes have been drill tested (of which only three have assay results available) out of 29 occurrences identified to date in outcrop and subcrop. Drilling results have consistently intersected broad copper mineralisation at or near surface including: 116m @ 2.4% Cu & 7.2g/t Ag (from 30m at the Cughur prospect); 72m @ 1.2% Cu & 8.8g/t Ag (from 14m at the Gaans prospect); and, 168m @ 0.74% Cu & 5.4g/t Ag (from 76m for the first hole at the Aranjin prospect) with higher grade intercepts of chalcocite and chalcopyrite mineralisation indicating potential primary mineralisation (eg 50m @ 3.5% Cu & 10.8% Ag and 34m @ 3.9% Cu & 14.7 g/t Ag respectively).

Ocean Comment

Voyager is looking to undertake a four part strategy at the KM project:

i. defining a maiden resource, the majority of which will be from the Gaans, Cughur and Aranjin prospects, and completing initial metallurgical analysis by Jun’Jul’12;

ii. determining the potential of the remaining 26 near surface hydrothermal breccia pipes already identified;

iii. gaining an understanding of the potential for a primary source of mineralisation; and,

iv. beginning feasibility studies/permitting for a +3Mtpa operation. The definition of a maiden ~30Mt @ ~1% Cu resource, with anticipated favourable met analysis, the majority of which will be from three near surface hydrothermal breccia pipes, is expected to be a transitional point for Voyager as it provides visibility for an attractive medium scale development project whilst highlighting the exploration upside of the remaining 26 largely untested near surface breccia pipes (let along the potential for a larger primary source of mineralisation or further near surface pipes).

The Company has completed +40,000 metres of drilling as part of its 50,000 programme for the first 10 months of exploration at KM. Voyager has stated an exploration target of 50-150Mt @ 0.8-1.5% Cu for the hydrothermal breccia targets (excluding the larger porphyry target). We expect a maiden resource in the order of 20-40Mt @ 0.80-1.20% Cu (mid range of ~300,000t contained copper) to be announced in Jun/Jul’12. The definition of a number of near surface hydrothermal breccia resources offers the potential for an attractive initial development project with a Pre-Feasibility Study (‘PFS’) and mine permitting expected to commence shortly. Recently Voyager has begun a separate drilling programme to test the high possibility of a primary source of mineralisation feeding the identified hydrothermal breccia pipes with initial drilling and analysis being encouraging.

Not many juniors complete this level of drilling within 10 months on an initial discovery. To help put Voyager’s exploration efforts and initial resource target into perspective we highlight Sandfire Resources’ and Rex Minerals who within a year of discovery defined maiden resources of 7.13Mt @ 5.2% Cu (contained copper of 372,000t) and 100Mt @ 0.7% Cu (700,000t copper) at their DeGrussa and Hillside projects respectively. Exploration results, definition of maiden resources and further exploration targets supported a significant re-rating in both Sandfire and Rex’s share price over this period of aggressive drilling. Voyager's first phase 50,000 metre drill programme testing only five prospects of the 29 hydrothermal breccia pipes identified to date, and its exploration target of 50-150Mt @ 0.8-1.5% Cu (contained copper of 400,000-2,250,00t), certainly places it in a comparable league in terms of initial exploration activities and contained resource/metal targets as Sandfire and Rex, two of the most successful ASX listed copper juniors of recent times.

News Flow & Catalysts

The Company continues to de-risk its flagship project as it gains a better understanding of the deeper primary mineralisation potential. We expect future potential discoveries of additional near surface mineralised pipes, initial metallurgical analysis, initial results of deeper drilling results testing the potential for a significant primary source of mineralisation, and the definition of a maiden JORC resource to be positive share price catalysts. In our view the maiden resource will support a ~3Mtpa operation potentially producing ~30,000tpa Cu for 10 years and expect the upcoming PFS to explore multiple development scenarios: a 3Mtpa operation; 5Mtpa operation; and, a blue sky 10Mtpa operation (the later two scenario’s highlighting the potential opex and capex of a larger development project which is possible with further exploration success and funding).

Voyagers’ KM and Khonger projects are situated in one of the most exciting and under explored copper belts in the world. Activities to date at KM and Khongor support medium term exploration targets of 50-100Mt @ 0.8-1.5% Cu and 100-200Mt @ 0.7-1.0% Cu respectively. Subject to exploration results confirming the Company’s targets, Voyager has the potential to be the next significant scale copper exploration/development play and offers unique exposure to Mongolia with a proven management team.

Centerra Gold Expects To Have A Busy 2012 -- President & CEO

Toronto, March 6 (Kitco News)–Centerra Gold Inc.’s (TSX:CG) president and chief executive officer, Stephen Lang, expects 2012 to be a busy year for the Canadian-based gold mining company.

Lang spoke to Kitco News at the PDAC2012, the Prospectors & Developers Association of Canada’s annual convention, which occurs from Sunday to Wednesday in Toronto.

“2012 will be a pretty busy year for us. I think particularly as we come out of the Mongolian elections, looking to get the approvals for Gatsuurt finally moving,” said Lang. “Once that happens it’ll take about two months for that to get into production and that’ll bring (the mine in) Mongolia where its historically been for us at the 150,000 to 200,000 ounce a year level.”

Lang also said that the company will be focusing on its Kumtor mine as well as a few other development projects.

“Meanwhile (we’re) also continuing to advance at the underground at Kumtor, looking to get into ore there in the second quarter of next year,” Lang said.

He added that the company is looking to further explore its Kara Beldyr, same at ATO mines.

“Both (went) into resource at the end of last year,” Lang said.

Centerra had a brief issue with its Kumtor mine, located in the Kyrgyz republic, when workers went on strike last month. They returned to work about a week later.

“We’re back to work there,” said Lang. “That really stemmed from a change in the taxation where there was a larger portion of the employee’s wages that were taken out for the social fund contribution to the country and just trying to come up with an agreement, some kind of a mechanism that could make that less painful for the employees.”

“But we’re back to work now and back to production.”

The company’s 2011 gold production totalled 642,380 ounces, down from 678,941 ounces in 2010. The lower production was attributed to the company’s Boroo mine production dropping nearly 50%.

“That’s really at the end of its mine life,” said Lang.

Boroo has produced about one million and a half ounces since we opened it in 2004, he added.

Denison Mines Corp. Reports 2011 Results

TORONTO, ONTARIO--(Marketwire - March 8, 2012) - Denison Mines Corp. ("Denison" or the "Company") (TSX:DML)(NYSE Amex: DNN) today reported its financial results for the three months and year ended December 31, 2011.

The Company recorded a net loss of $65,537,000 or $0.17 per share for the three months ended December 31, 2011 compared with a net loss of $9,394,000 or $0.03 per share for the same period in 2010. The net loss for 2011 includes a non-cash impairment charge of $32.6 million against goodwill in its U.S. mining segment in the fourth quarter. For the year ended December 31, 2011, the Company recorded a net loss of $70,869,000 or $0.19 per share compared to a net loss of $5,346,000 or $0.02 per share for the same period in 2010.

…

Operating Highlights

· Denison's 2011 production totaled 1,011,000 pounds uranium oxide ("U3O8") and 1,290,000 pounds of vanadium blackflake ("V2O5").

· During the year Denison acquired White Canyon Uranium Limited ("WCU"). WCU's key assets are located in southeastern Utah, near Denison's White Mesa mill. Its holdings comprise 100% interests in the Daneros uranium mine which is currently in production, the advanced Lark Royal project and the Thompson, Geitus, Blue Jay and Marcy Look exploration projects.

· The Company continued development of its Pinenut mine in Arizona. Production is expected to commence in mid-2012.

· The Company continued drilling at its 60% owned Wheeler River exploration property in Saskatchewan. The 2011 summer drill program focused primarily on Zone A and was very successful in expanding the potential estimated resources of the Phoenix deposit with the discovery of the "Zone A Extension".

· In Zambia, the Company completed a successful two-phase drilling program at its 100% owned Mutanga uranium project. Based on the results of this drilling, a new inferred resource estimate for the Dibwe East deposit, compliant with National Instrument 43-101 ("NI 43-101"), was announced on February 27, 2012 totaling 28.2 million pounds U3O8.

· In Mongolia, mining licence applications were submitted on four of the five Gurvan Saihan Joint Venture licence areas.

…

Mineral Property Exploration

Exploration expenditures of $200,000 for the three months ended December 31, 2011 ($129,000 for the three months ended December 31, 2010) and of $3,971,000 for the year ended December 31, 2011 ($970,000 for the year ended December 31, 2010) were incurred in Mongolia on the Company's joint venture properties. The Company has a 70% interest in the Gurvan Saihan Joint Venture ("GSJV") in Mongolia. The other parties to the joint venture are currently the Mongolian government as to 15% and Geologorazvedka, a Russian entity, as to 15%. Under the Nuclear Energy Law, the Government of Mongolia's position in the joint venture will increase from its current 15% interest to a 34% to 51% interest, depending on the amount of historic exploration that was funded by the Government of Mongolia, at no cost to the Government. This share interest will continue to be held by Mon-Atom LLC, the Mongolian State-owned uranium company. The Company and Mon-Atom are proceeding with restructuring the GSJV to meet the requirements of the Nuclear Energy Law, pending government reviews and authorizations. In November 2011, in preparation for this restructuring, the Company finalized terms for acquisition of the Russian participant's share in the GSJV. Subject to receipt of required approvals, this 15% share interest will be acquired by the Company for nominal cash consideration and release of the Russian participant's share of unfunded joint venture obligations.

…

Outlook for 2012

…

Business Development

…

In Mongolia, a $4.1 million exploration and development program is projected, contingent upon receipt of the mining licences in mid-2012. Included in this budget is a $1.6 million, 17,500 metre exploration program focused on the Ulziit and Urt Tsav 2011 discoveries. The development activities will include design of the pilot plant and infrastructure.

…

Khan Mongolia Equity Fund: An Interview With Travis Hamilton

March 4 (Jon Springer via SeekingAlpha) The Khan Mongolia Equity Fund is open to investors worldwide, including the United States. The minimum investment is $50,000 for accredited investors.

Travis Hamilton founded Khan Investment Management Limited in March 2011 and launched the Khan Mongolia Equity Fund in October 2011. The fact sheet for the fund states: "The Khan Mongolia Equity Fund is the preeminent investment vehicle for investors who seek a diversified and liquid exposure to one of the world's most resource rich and fastest growing economies."

Mr. Hamilton previously worked for the Helvetica Group where he was an Executive Director at Helvetica Wealth Management Partners (Asia) Pte and Helvetica Australia Pty Ltd. He recently appeared on Bloomberg television and the BBC to discuss Mongolia and the Khan Mongolia Equity Fund.

1 - How did you come to be interested in investing in Mongolia?

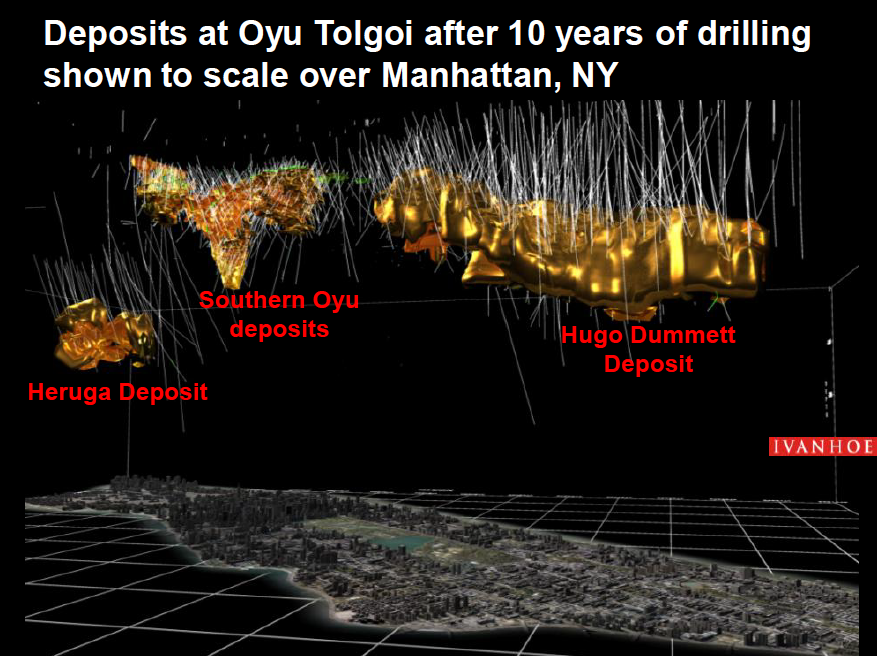

Mr. Hamilton: By chance I was first made aware of the vast opportunities in Mongolia at a cocktail party in Beijing in 2006. There I was introduced to an incredibly engaging chap who spoke passionately about Mongolia: a tiny frontier market with masses of mineral wealth on China's doorstep. I was chatting with Robert Friedland, CEO of Ivanhoe Mines (IVN). Based on that chat alone, I knew there must be some exciting opportunities beyond the Oyu Tolgoi, and decided to undertake some independent research of my own. [Mr. Friedland's Ivanhoe Mines in 2006 knew what they had in the Oyu Togloi and Bronze Fox copper-gold mines.]

Source: Ivanhoe Mines November 2011 corporate presentation.

2 - So, you began to invest in Mongolia then?

Mr. Hamilton: No. I was in China for business at the time. When I returned to Singapore (my home since 2002) I began investigating what opportunities were available for offshore investors to gain exposure to this nascent market. Disappointingly, I didn't discover much at all, beyond simply buying Ivanhoe. Whilst Ivanhoe represented a good "first step" I was looking for a more diversified exposure. Whilst I maintained a keen interest in Mongolia and developments there I was preoccupied managing Helvetica's Asian business and had little time to dedicate to my interest in emerging and frontier markets. Then, along came the "GFC" [global financial crisis] and my commitments at Helvetica became all consuming.

Fast forward to 2010. Due to a material change in strategy that I could not align myself with, I decided to leave the Helvetica Group and at the end of August began six months of "gardening leave". The timing couldn't have been better. I decided to use this time to investigate further the various Asian frontier markets that had piqued my interest previously. Among several other countries, Mongolia was a must-see firsthand.

Source: The World Bank's Mongolia Quarterly Economic Update, February 2012.

In November 2010 I traveled to Ulaanbaatar [UB] with a number of Australian investors to review a pre-IPO capital raising opportunity for a Mongolian conglomerate that was hoping to list on the Hong Kong Stock Exchange the following year. Whilst in UB, I took the opportunity to meet with a number of other companies, investment advisers, banks and brokers. I was keen to open a local account and gain some exposure to the Mongolian Stock Exchange. I found the process of opening a local brokerage account at that time though seemed onerous, and I had a number of concerns about the potential advice I would receive, the lack of transparency around trading and the seemingly poor liquidity of the market.

I asked all of the brokers and dealers I met with "why is it so challenging for an offshore investor to gain some exposure to this market" particularly given that in my mind, most investors would only be allocating a small portion of their portfolios to such a tiny frontier market, and wouldn't be bothered with going through the hassles of opening onshore accounts.

"Why don't you have a fund? An offshore collective investment vehicle that international investors can simply acquire through their private banking or broker relationships?"

Their responses were unanimous: "Everyone asks us that!"

I realized that these chaps were dealers and brokers. They did not have the experience, the expertise, nor the motivation to create an offshore investment vehicle that could provide international investors with liquid, onshore Mongolian equity exposure.

Upon returning to Singapore I confirmed through further investigating that indeed no such structure as I had perceived existed. After floating the idea with a number of private investors that I had known since my Credit Suisse days, it was clear that I was not alone in seeking such an investment structure. Here was a need that I could fulfill.

3 - Then why didn't you start a fund that only invests in the Mongolian Stock Exchange?

Mr. Hamilton: The MSE to date remains extremely small and continues to face liquidity challenges. Furthermore, I believe that the Mongolian growth story extends beyond companies that are listed in Mongolia. The Board A of the MSE has 36 stocks, and of these we really only look at small number as potential investments (to date we have invested in 4). The market capitalization of the MSE top 20 is under USD 1.6 billion. Conversely, we have identified 64 companies listed on international exchanges that have substantial operations and / or assets in Mongolia. The combined market capitalization of these companies listed internationally extends beyond USD 40 billion.

Having said that, given the London Stock Exchange's management and modernization of the MSE, important changes to the regulatory framework and the Government's proposed privatization plan for many state owned enterprises (SOEs) - a large number of which are expected to be privatized through IPOs on the MSE - I believe that there are clearly significant opportunities for investing in the local exchange over the months and years to come. In fact, Bold Baatar, Chairman of the MSE, announced in October 2011 at the Mongolian Investment Summit in Hong Kong, that he foresees a potential IPO pipeline on the MSE in excess of USD 40 billion over the next 5 years.

Don't get me wrong. The Khan Mongolia Equity Fund is positioned to provide investors with onshore equity exposure.

However, based on my experience from 2008 and 2009, having worked extensively with high net worth individuals, private investors now demand investment vehicles that offer liquidity. You simply can't lock investor's capital up for years. Previously investment managers were able to launch closed-end structures, and then list them on exchanges in the guise of offering liquidity. The GFC proved that this does work.

Furthermore, as I believe the Mongolian growth story is an opportunity that will continue to attract capital for the next several years, I didn't want to limit the period of time that I had to raise capital.

Hence, we launched an open-ended investment fund whereby investors can subscribe or redeem their shares at an independently audited Net Asset Value every month - without bid / offer spreads and substantial discounts to the true value of their investment.

Providing investors with monthly dealing - the ability to subscribe or redeem - means that liquidity management is key for us. We have to approach our investing from a liquidity management perspective. This is the second reason why our portfolio blends on-shore with off-shore listed securities.

4 - Okay. The Mongolian Stock Exchange as it stands is not very liquid at all. It can take weeks to build positions as a small investor, let alone as an investment fund. Does that mean you are limiting exposure to the Mongolia Stock Exchange?

Mr. Hamilton: No. Among the fund's current 16 positions, close to 30% of assets are invested in the Mongolia Stock Exchange at this time. Thanks to our extended onshore network we are regularly presented a number of off-market opportunities to acquire large blocks of stock.

Source: Eurasia Capital's Mongolia Outlook 2012 (published January 31, 2012).

5 - To be clear then, what are the Khan Mongolia Equity Fund's objectives?

Mr. Hamilton: The fund's objective, as stated in the Offering Memorandum, is to capture the opportunities for growth offered by the expanding Mongolian economy by investing primarily in equity securities of Mongolian companies.

Having had our Offering Memorandum written from scratch (at considerable expense) I wanted to make sure however that we didn't close the door on any potential investment opportunities. On that basis, the fund is not restricted with regards to its investment remit. We can be 100% cash or 100% invested. We have the ability to invest in private equity and pre-IPO opportunities. We can invest in debt instruments.

We invest both on-shore in Mongolia and offshore, outside of Mongolia, in any assets that are principally Mongolian investments. We may also invest in the Mongolian bond market, real estate, or any other investment as long as it is " Mongolian", and meets our investment guidelines.

Source: The World Bank's Mongolia Quarterly Economic Update, February 2012.

Whilst our remit is wide, I'd like to highlight again, that liquidity management for us is key. We obviously can't invest heavily into private equity if we are offering investors monthly liquidity.

We have soft concentration guidelines to invest no more than 10% in a single issue at acquisition and typically not to allow a single issue to appreciate beyond 15% of the fund.

We asses pre-IPO and IPO opportunities regularly.

We do not short. We do not use options. We do not use leverage. We do hedge our non-MNT currency exposure back to USD, as we are not trying to make money by trading currencies. We don't hedge MNT exposure, as ultimately we are bullish on the currency. Essentially, we are an unleveraged big beta play on Mongolia.

With regards to returns, we are seeking to provide investors with a multiple of GDP growth.

6 - Can you give examples of your IPO participation and opportunities?

Mr. Hamilton: We recently participated in the FeOre (FEO.AX) IPO in Australia that is an iron ore mining company with properties in Mongolia. At the same time, our investment committee reviewed and rejected another recent IPO in Canada because it didn't meet the standard of our fund. We analyzed and subsequently subscribed to a third IPO, however it is yet to come to market.

We are contacted regularly about IPO opportunities. We research each opportunity on its individual merits with an eye to how it fits into the fund's investment profile and objectives.

We are seeing a number of assets that are likely to come onto the ASX in particular over the coming months.

7 - Who is on your investment committee?

Mr. Hamilton: There are five people on the investment committee. 2 representatives from our Investment Advisor, Monet LLC [a Mongolian brokerage house and investment bank], 2 representatives from Khan (including myself), and the Managing Director of our Investment Manager, Gordian Capital Singapore.

After a lot of meetings in Mongolia, we settled on Monet Capital as our local investment advisor in Mongolia. Fiezullah Saidov, their head of investment banking, and Oliver Belfitt-Nash, their head of research, are two members of our IC. Monet undertakes independent research on companies listed, or soon to be listed, both on-shore and offshore, and they provide us with investment rationales, based on their unique insight, for any investment that we are considering for the fund.

In additional to our partnership with Monet, we have relationships with four additional brokerages houses in Mongolia in order to ensure market coverage and to provide access to new and secondary issues as they come to market.

Also on the investment committee to provide a local view independent from our investment advisor we have "Nick" Narantuguldur Saijrakh formerly from Asia Pacific Securities, the brokerage division of Asia Pacific Investment Partners. Nick, who is a Director of Khan Investment Management, is essentially Khan's independent eyes and ears on the ground in Mongolia.

Lastly, we have appointed Gordian Capital Singapore as the investment manager of the fund. Gordian, a licensed investment manager under the Monetary Authority of Singapore, undertakes the legal and risk management responsibilities for the fund, whilst delegating the investment advisory function to Khan & Monet. Gordian's Managing Director, Mark Voumard is the 5th and final member of our investment committee.

8 - I would like to compare your fund to two other Mongolia investment funds, the Quam Silk Road Mongolia Fund and the MSE Liquidity Fund. How do you compare to Quam?

Mr. Hamilton: The Quam Silkroad Mongolia Fund is a very different structure to the Khan Mongolia Equity Fund. Firstly, the Quam Fund is a segregated investment portfolio of Quam Funds Limited, which is an umbrella structure covering a number of strategies and portfolios. Our fund has been structured as a stand-alone single entity and thus avoids any potential contagion issues that may be raised through a structure such as Quam's. A number of "blow-ups" during the GFC highlighted issues associated with umbrella structures, and personally I avoid them.

Beyond that, we have very different fee structures and operate in differing investment universes.

The basis of their fund is the global Silk Road Mongolian Index (not investable), which is a market capitalization based index of the largest listed companies with assets or operations in Mongolia.

Source: Eurasia Capital's Mongolia Outlook 2012 (published January 31, 2012).

As their portfolio composition seems to be dictated by market capitalization of the companies within the Silk Road Mongolian Index, they do not have any concentration limits with regards to exposure, and I understand their portfolio is heavily weighted to two individual positions. Furthermore, I am not aware of any onshore investments that they have made in Mongolia, and am unaware of their ability to participate in the IPO market.

I was informed recently that the former portfolio manager Richard Harris has left Quam in January of this year. I am not sure if the new portfolio manager Simon Potter will change the investment strategy, or stick with the status quo.

[Interviewer note: This September 2011 article from Frontier Securities indicates the fund had 43% invested in its top position, Ivanhoe Mines, at that time.]

9 - And the MSE Liquidity Fund? As I understand it, the MSE Liquidity Fund is the opposite of the Quam fund, as it only will invest in Mongolia with a minimum exposure of 30% to Certificates of Deposit in Mongolia; and a minimum 30% exposures to equities on the Mongolia Stock Exchange; and with management allowed to choose between equities and CDs with the remaining 40%.

Mr. Hamilton: Again, the MSE Liquidity Fund is a very different type of investment vehicle which offers investors a different type of exposure to Mongolia. We have differing fee structures, liquidity terms and investment universes.

With a very low minimum investment of USD 10,000 they have something different to offer international investors. We know and like several of the team members over there at Origo and ResCap. They are investing exclusively on-shore in Mongolia, whereas we invest on-shore and offshore in any Mongolia related investment. They are essentially different products with differing demands.

10 - Let's discuss fees for a moment. Your fund has a one-time 1.5% subscription fee, a 1.5% annual management fee, and a 10% performance fee with a high water mark. Additionally, there is a 5% redemption fee if redemption is in less than 12 months. The performance fee will only be taken once per year on June 30. My calculations rendered this chart that I based on $10,000 investment for ease of viewing although your minimum investment is $50,000.

Principal | Fund's Gains | Subscribe Fee | Mgmt Fee | Perform Fee | End Value | Real Return |

$10,000 | 10% (1st yr) | $150 | $147.75 | $97.02 | $10,575.45 | 5.75% |

$10,000 | 20% (1st yr) | $150 | $147.75 | $194.05 | $11,488.66 | 14.49% |

$10,000 | 30% (1st yr) | $150 | $147.75 | $291.07 | $12,321.86 | 23.22% |

$10,000 | 50% (1st yr) | $150 | $147.75 | $485.11 | $14,068.26 | 40.68% |

$10,000 | 70% (1st yr) | $150 | $147.75 | $679.16 | $15,814.67 | 58.15% |

11 - Is that accurate?

Mr. Hamilton: All of the performance numbers we publish are NET of fees and expenses.

Assuming that the above gains were on a GROSS basis, yes, the NET return could be roughly approximated by your calculations, however, it is important to note that the management fee is levied on NET Assets Under Management per month. Your calculations assume that the 1.5% management fee is deducted in entirety before any performance is made.

12 - The fund ran a 6.32% loss from October through the end of the year last year. Why choose your fund over the other ways to invest in Mongolia?

Mr. Hamilton: The Khan Mongolia Equity Fund is the only investment fund that combines experienced local on-shore investment expertise with efficient offshore structuring to provide global investors a diversified and liquid exposure to Mongolia. We have appointed industry leading service providers and developed key relationships with multiple brokers and underwriters, both locally and internationally in order to achieve our capital growth objectives. We emphasize and offer liquidity. We have the reach and scope to make purchases globally.

Mongolia's growth story is going to go the rest of this decade and probably longer. Oyu Tolgoi will start production later this year, and will be ramping up production through to 2020. The Tavan Tolgoi IPO is expected this year, and its IPO on the MSE will about double the size of the local market. We expect $40 billion in Mongolian IPOs in the next few years. The number one performing stock market in the world in 2010 was Mongolia. The number two performing stock market in the world in 2011 after Venezuela's was Mongolia.

We believe our fund will be the best way to securely invest in Mongolia for the next five to seven years, after which point we anticipate more efficient ways for investors to gain a diversified exposure to Mongolia. At that time we may shift the fund's style and objective, but that is some time away.

13 - Returning to the fund's outlook. The economic boom in Mongolia is the mining industry. How much of the fund is focused on mining compared to how much is focused on other sectors? Will you try to cap the fund's allocation to mining investments at a certain level? Or, can you talk about the non-mining assets and how you value them in the portfolio compared with how you value and weight the mining assets in the fund's portfolio?

We are not restricted by any allocation limits to specific industries or sectors. When investing in the Mongolian growth story, its fair to say though that its hard to avoid the mining sector and mining related industries. Having said that, the significant amounts of investment that have been made in the mining sector over the last several years are already providing significant spillover effects into other areas of the economy.

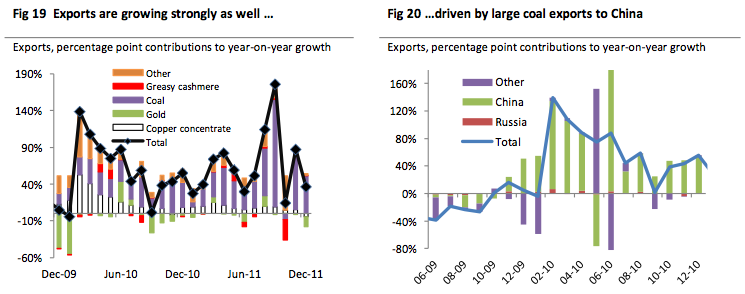

Source: Eurasia Capital's Mongolia Outlook 2012 (published January 31, 2012).

Presently, slightly over half of our portfolio is allocated across various mining exploration, development and producing companies. We have a significant exposure to building materials, consumer staples, and logistics. We foresee opportunities in the coming months to diversify further into financial services, power generation and distribution as well as other companies that will leverage the construction and infrastructure development sectors. We will also be reviewing and potentially investing in additional exploration, producing and mineral processing assets.

14 - One of the biggest challenges in Mongolia is building up the infrastructure to be able to export from their mining operations, and down the road to be able to make finished products from their mining operations. What makes you confident in Mongolia's infrastructure development?

It's still very early days for this nascent economy. As the old adage says "Rome wasn't built in a day", and I think we need to measure our expectations and not forget that it wasn't that long ago that GDP per capita was less than USD 500, almost half of the economy was driven by agriculture, and very few people in the first world had ever considered investing in this former Soviet outpost.

Growth of the economy will remain dependent on attracting additional foreign investment for some time to come. It's the role of the Government to ensure that the right policies and legislative framework remain in place to attract investment for infrastructure development. The private sector is already planning and building the additional infrastructure it requires from power plants to roads. Once the Government coffers begin to fill, following the start of production at Oyu Tolgoi & Tavan Tolgoi, I believe that they will be quick to undertake their own infrastructure initiatives. The wheels are in motion, and I'm confident that in time, the required development will come - just not in a single summer.

15 - Some investors are concerned that Mongolia is dependent on China, as over 80% of Mongolia's exports already go to China, and that China's economy slowing down will curtail Mongolia's economy and GDP growth. What is your outlook on China's economy, and Mongolia's economic relationship with China going forward?

Mongolia and China are unquestionably linked - Mongolia has the assets, China has the appetite.

I have no concerns whatsoever though that European sovereign default, US recessions or a significant slowdown in China are going to derail the current growth forecasts for Mongolia. Let's put things into perspective for a moment. Market commentators are concerned about a slowdown in China when real GDP growth figures come in at 9.1% y-o-y, comparative to a forecast of 9.3% - give me a break! Let's assume for a moment that Chinese growth halves - which personally I don't see happening. No - let's say growth goes to zero.

Even then, the only impediment at present preventing China from acquiring more resource inputs from Mongolia instead of the comparatively more expensive seaborne inputs from Australia, India and Indonesia is the lack of infrastructure in place to transport Mongolia's vast mineral wealth across the border. Furthermore, the large mining projects are yet to hit production.

Source: Eurasia Capital's Mongolia Outlook 2012 (published January 31, 2012).

The big mining companies have passed the point of no return - they have invested billions of dollars to bring their projects to production. Some estimates indicate that Rio Tinto (RIO) and Ivanhoe will have spent USD 7 billion before they flick the "on" switch at Oyu Tolgoi. These are sunk costs. Even with downward pressure on prices, so long as they are producing at a variable cost lower than their selling price, they will go on producing. And that means that the flow on effects to rest of the economy will continue.

Let's also not forget the absolute numbers we're talking about here. 2010 GDP in Mongolia was USD 6.4 billion. Preliminary estimates of 2011 GDP are USD 8.6 billion. These are tiny numbers, and are completely insignificant when compared to Mongolia's Southern neighbor.

In addition to feeding Chinese consumption, there are also plans afoot that are likely to open up additional export markets for Mongolia's mineral resources over the coming years.

These are still very early days for Mongolian growth, and I only see the pace intensifying over the coming years.

Thank you for your time Travis. Readers who wish to contact Travis about investing in his fund can reach him at:travis.hamilton@khan-management.com

Note To Readers: Graphics from the World Bank's February 2012 Mongolia Quarterly Economic Update and from Eurasia Capital's Mongolia Outlook 2012 (published January 31, 2012) are cited often herein because they are the most recent comprehensive reports on Mongolia at the time of publication.

Mongolia Growth Group Ltd. Publishes February 2012 Monthly Letter to Shareholders

Ulaanbaatar, MONGOLIA, Mar 05, 2012 (FSC) -- Mongolia Growth Group Ltd. (YAK - CNSX),is pleased to announce the release of its February 2012 letter to shareholders.

February 2012 Shareholder Letter

To the Shareholders of Mongolia Growth Group Ltd.,

I would like to start the February letter by mentioning that we will be holding our annual general meeting on April 14th at 2:00PM at the Westin Harbour Castle, 1 Harbour Square, Toronto, ON M5J 1A6. Please email Genevieve Walkden at Gwalkden@mongoliagrowthgroup.com if you are interested in attending. Naturally, we look forward to seeing as many of you as possible.

February saw two big events for our company. The first of these was the one year anniversary of the founding of MGG. I don't need to reprise all that has happened in our first year, but a few key bullet points should be sufficient.

-Listed MGG and grew from 2 employees to 61 today

-Raised CDN$51.5 million to pursue our investment objectives in year one.

-Acquired 32.8B MNT worth of investment property in Ulaanbaatar

-Partnered with UMC to create Mandal General Insurance, our insurance company

Naturally, the hardest steps for any company are those foundation steps in the first few months. We now feel confident that we have the management team and capital to pursue our objectives in our second year of operations.

The other big event was that our property company has now joined Mandal Insurance in the soon to be re-named Mandal Building on Seoul Street. Having the whole family under one roof should greatly help communications and our future growth.

February was something of a slower month from a property acquisition perspective as we were focused on our move and also the celebrations for Mongolian Lunar New Year, Tsaagan Sar. As we transition to acquiring larger properties, the due diligence timeframe seems to expand. Based on our pipeline, we anticipate that March will see a number of closings for us as some transactions were delayed due to the holiday.

With that, I'd like to leave you with a few images from our ribbon cutting as we moved into our new headquarters. This will be followed in the spring with the formal renaming ceremony for the building after our renovations are completed.

Sincerely,

Harris Kupperman

Chairman & CEO

Mongolia Growth Group Ltd.

Solartech Interim Results 2011-2012

March 9, Solartech International Holdings Limited (HK:1166) --

---

11. DEPOSIT FOR ACQUSITION OF AVAILABLE-FOR-SALE FINANCIAL ASSET

On 5 July 2011, the Group entered into a sale and purchase agreement with Hero Wisdom Limited (the “Vendor”), pursuant to which the Company has conditionally agreed to acquire from the Vendor its 10% equity interest in Venture Max Limited (“VML”), a company incorporated in the British Virgin Islands which holds mining and exploration licences in the State of Mongolia through Mongolian Copper Mining LLC, VML’s wholly-owned subsidiary incorporated in the State of Mongolia (the “First Proposed Acquisition”). The consideration of the First Proposed Acquisition is HK$100,000,000, of which the Group paid HK$50,000,000 as deposit upon signing the agreement. The completion of the First Proposed Acquisition is subject to several conditions and up to 31 December 2011 and the date of this report, the First Proposed Acquisition has not yet been completed and further details are set out in the Company’s announcement dated 5 July 2011.

…

Mining

During the period under review, the business of the Group’s copper-gold-silver mines in Mongolia included additional exploration and site surveying, such as road transport planning, power supply laying works and search for closer water sources for the proposed ore processing plant. The Mongolian team of the Group is currently preparing the relevant documents for delivery to the State authority for obtaining the required written consents, permits, approvals and agreements before commencement of operation. Unstable weather, shortage of professional staff and increased demand for relevant equipment in Mongolia have certain impacts on the progress.

The Group expects to complete the acquisition of 10% of the issued shares of another Mongolian mining company in the second half of the year. The Group expects that its competitiveness will be enhanced through the synergy created between the Mongolian mining company under this acquisition and the existing mining business of the Group by reducing operating costs, providing beneficial conditions for the Group’s business in Mongolia and leveraging on the vast human relationship network of the substantial shareholder of the Mongolian mining company in Mongolia.

…

DISCLOSEABLE TRANSACTIONS

Acquisition of 10% of the total issued share capital of Venture Max Limited

On 5 July 2011, the Company and Expert Assets Management Limited (“Expert Assets”), an indirect wholly-owned subsidiary of the Company), entered into a sale and purchase agreement (the “Agreement”) with Hero Wisdom Limited (the “Vendor”) and Mr. Batmunkh Dulamjav (the “Guarantor”) pursuant to which Expert Assets conditionally agreed to acquire from the Vendor ten issued Shares (the “Sale Shares”) of Venture Max Limited (“Venture Max”) (the “Acquisition”), representing 10% of the total issued share capital of Venture Max upon completion of the Acquisition. Venture Max is a company incorporated in the British Virgin Islands and was directly wholly-owned by the Vendor.

Venture Max holds the entire equity interest in Mongolian Copper Mining LLC (“MCM”) which is a company incorporated in Mongolia with limited liability and the holder of the Minerals Exploration Special Licence 5481X. The consideration for the Sale Shares payable under the Agreement is HK$100,000,000 and shall be satisfied by Expert Assets by (i) payment of HK$50,000,000 in cash as a deposit upon signing of the Agreement and (ii) payment of HK$50,000,000 in cash at completion of the Acquisition. The Vendor is directly wholly-owned by the Guarantor. The Vendor and the Guarantor are third parties independent of the Company and its connected persons.

The Company has been seeking suitable opportunities to facilitate its ongoing expansion into the mining business and the Directors believe the Acquisition represents such an opportunity. The completion of the Acquisition is conditional on the conditions in the Agreement being satisfied or waived on or before 10 March 2012. Details of the Agreement and the Acquisition, which constitutes a discloseable transaction under the Listing Rules, were set out in the announcement of the Company dated 5 July 2011.

…

Mongolia Will Gain Access to the World Bank’s IBRD Financing

Ulan Bator, March 7, 2012 (World Bank) – Following a careful review of Mongolia’s development opportunities, the World Bank has decided to declare Mongolia creditworthy for its International Bank for Reconstruction and Development (IBRD) lending.

“As Mongolia’s development needs remain great, the government is seeking to access new sources of financing to accelerate critical investments” said Mongolia’s Finance Minister D. Khayankhyarvaa. “We are pleased that the World Bank, which has been a strong partner of Mongolia over the past twenty years, has decided to extend additional support to Mongolia through its IBRD financing.”

“With our financial and analytical support, Mongolia has been able to achieve some excellent results – bringing water to the ger areas of Ulaanbaatar, helping set up mobile phone services across the country, and establishing more transparent and effective public management systems. We are confident that they will continue to make good use of IBRD resources” said Klaus Rohland, World Bank Country Director for China and Mongolia.

The World Bank Group makes IBRD financing available to middle-income and creditworthy poorer countries to promote sustainable, equitable and job-creating growth, reduce poverty and address issues of regional and global importance. IBRD clients gain access to capital on favorable terms in larger volumes, with longer maturities, and in a more sustainable manner than world financial markets typically provide. Unlike commercial banks, IBRD is driven by development impact rather than profit maximization.

Mongolia will continue to qualify for concessional financing from the International Development Association (IDA), the World Bank fund for the poorest, during a transition period.

To know more about IBRD, visit http://treasury.worldbank.org/bdm/htm/index.html

To know more about the impact of IDA-funded projects in Mongolia, visit http://www.worldbank.org/en/country/mongolia/projects/results

Salary and pension increases

March 7 (news.mn) Today’s plenary session of parliament approved amendments to the Budget law for 2012 and Law on Social insurance fund. An amendments will be effective since February 1, 2012. It means salary of state workers and pension for elderly people will increase since February 1. According to the previous decision salary and pension should be increase by stage- first beginning from February 1, second from May 1. By the amendments state budget expanded by Tg161.5 billion, social insurance fund by Tg13.9 billion.

Total budget income increased to Tg 6 trillion 3.6 billion, expenditure to Tg 6 trillion 467.7 billion and budget loss will 3 percent of GDP.

ROADS TO BE CONSTRUCTED IN KHOVD

Ulaanbaatar, Mongolia, March 7 /MONTSAME/ Paved-roads will be run between Baga ulaan davaa (mountain pass) and Mankhan soum of Khovd aimag (103.3 km) and in localities (20 km).

These roads are to receive a soft loan of USD 45 million for the #1 project at an investment program on developing auto roads of the vertical axis.

The credit agreement on the soft loan will be established between the government of Mongolia and the Asian Development Bank (ADB), and it will be signed by D.Khayankhyarvaa, the Minister of Finance, the cabinet decided. In a scope of the project, one fully-equipped unit of repair works will be set up.

The term of the soft loan is 32 years, its primary payment will be done within eight years. The interest of the soft loan is one per cent within the term of the primary payment, to become 1.5 per cent after it.

The program on developing auto roads of the vertical axis is financed with USD 170 million from the ADB and with USD 92 million from Mongolia's government in three phases for 7-10 years.

In frames of the program, construction of another paved road of 293 km will be completed, and three units of repair will be set up. A construction of 34.9 km in localities and bridges will be done as well.

IMF: Mongolia: Second Post-Program Monitoring Discussions

March 7 (IMF) --

The following documents have been released and are included in this package:

· The staff report, prepared by a staff team of the IMF, following discussions that ended on September 20, 2011, with the officials of Mongolia on economic developments and policies. Based on information available at the time of these discussions, the staff report was completed on October 25, 2011 The views expressed in the staff report are those of the staff team and do not necessarily reflect the views of the Executive Board of the IMF.

· A Staff Supplement of November 8, 2011 updating information on recent developments.

· A Public Information Notice (PIN).

The policy of publication of staff reports and other documents allows for the deletion of market-sensitive information.

…

Preferred Signs its First Hotel (The Blue Sky Hotel & Tower) in Mongolia

March 7 (AsiaTravelTips.com) Preferred Hotels & Resorts has signed its first member in Mongolia – the brand new The Blue Sky Hotel & Tower.

The Blue Sky Hotel & Tower is a 200-room hotel housed within a newly built tower with a glass exterior - currently the tallest and most prominent building in Mongolia.

The hotel is located on the Sukhbaatar Square in the heart of Ulaanbaatar’s business centre with government agencies, entertainment as well as tourist attractions nearby.

Occupying the top floors of the tower, the rooms offer views of the city with understated design and warm earth tones. At present, it is the only hotel in the country with a dedicated executive floor, lounge and complete executive floor benefits.

Five restaurants offer Japanese, Chinese, Korean and European cuisines and other international favourites.

For entertainment, there is a lounge located on the top two floors of the tower and a separate club providing live bands and DJs.

Recreational facilities include an indoor climate-controlled pool, gymnasium, sauna and three large jacuzzi tubs of varying temperatures.

With one of the largest function spaces in the city fitted with state-of-the-art visual, acoustic and lighting equipment, Hotel Blue Sky can cater for various events for up to 500 persons within the two ballrooms and three function rooms.

To celebrate its opening, the hotel is offering a Buy One Get One Free promotion with rates from US$320 (US$160 per night) with free breakfast, free WIFI, and taxes included. The promotion is valid until 31 May 2012.

M.A.D.: Mongolian Real Estate Market - Overview, challenges and opportunities - VIDEO

March 5 (M.A.D. Investment Solutions) A brief overview of the current state of the Mongolian Real Estate market, with an exploration of its demand and supply factors as well as challenges and opportunities faced by foreign investors.

CHINA NPC: Anhui Conch Chairman: Indonesia Cement Project Still Awaiting Approval (and examining investment opportunities in Mongolia)

BEIJING, March 6 (Dow Jones)--Anhui Conch Cement Co. (600585.SH), China's largest cement producer, is still working to obtain final approval from the Indonesian government for its massive $2.35 billion investment in Indonesia, Chairman Guo Wensan told reporters Wednesday.

Speaking on the sidelines of the National People's Congress, Guo said talks to iron out the deal, announced in June last year, to set up four cement plants in the Southeast Asian nation are "proceeding smoothly."

Meanwhile, the company is examining other overseas investment projects in Brazil and Mongolia, among other opportunities, he said.

Comment: Mongolia’s Mining Wealth Should Not Limit School Opportunities

A guest commentary

March 8 (Eurasianet.org) Mongolia is using its newly exploited mineral wealth to reform its social services. While the government should be applauded for looking to the future, it is a challenge ensuring the changes don’t come at the expense of the majority of people in this vast and rural country. Mongolia’s unique population structure creates especially difficult conditions for schools, which are frequently over-crowded in the capital, Ulaanbaatar, but must accommodate sparse and highly dispersed populations elsewhere.

Mongolia’s approach to education reform appears to be quite similar to efforts in Kazakhstan, another natural resource-rich Central Asian state. Both countries are working with prestigious Cambridge University to develop a small network of elite schools that will serve the most academically successful students in the capital city and regional centers. The goal seems to be to develop schools to match their elite counterparts in developed countries quickly—a sort of superficial European renovation for the education system. Both countries also envision the good teaching practices that Cambridge consultants help develop and implement to trickle down to the rest of the education system.

But education reform does not trickle without a concerted effort and well-coordinated plan, which the Ministry of Education currently lacks. The government must also be willing to commit significant resources to build and equip new schools, renovate existing infrastructure, and train teachers. For example, class sizes in the elite schools are to be capped at 25 students with a teacher and teaching assistant. A typical school in Ulaanbaatar has class sizes upwards of 40 students per teacher with no teaching assistants. Even if teachers in typical schools receive additional training from the new program, it will be difficult for them to implement strategies designed for much smaller classes.

Ulaanbaatar-based NGOs dedicated to education worry that public schools lack adequate financing, teachers are poorly paid, schools and dormitories are severely under-resourced, and thousands of children don’t even attend school. They fear that the huge investment required by the new elite schools will divert resources from public schools.

Even without the challenges of scaling-up practices that are designed for well-resourced pilot sites, separating academically successful children into an elite system raises serious concerns about equity. Though Mongolia’s legislators have backed away from a proposal to charge fees for parents who send their children to the elite schools after civil society advocates raised concerns about discrimination against children from poor families, this type of two-tiered system is inherently discriminatory.

Selecting and sorting students based on narrow measures of academic achievement, like admissions tests, tends to deepen social inequalities by favoring children who have been well prepared through preschool programs and family experience. Thus, children living in poverty, children in rural areas without access to preschool, minority and minority-language children, and children with disabilities are at an immediate disadvantage, and certain not to test into the elite schools.

Research by the OECD shows that countries with greater equity in their education systems produce better outcomes for all children than those that sort and track their students. If education reform in Mongolia is to pave the way for prosperity and social cohesion, as the Ministry of Education promises, policies must direct resources to the children who need them most, not a small elite.

Editor’s Note: Kate Lapham is Senior Program Manager for the Open Society Education Support Program. ESP and EurasiaNet both operate under the auspices of the Open Society Foundations.

Norihiko Kato: The correct distribution of resources does not mean selling it at high prices, but making the right decision for future generations

March 7 (UB Post) This is an interview with the CEO of Khan Bank, Norihiko Kato, regarding the future economy and finance of Mongolia. Translated from Udriin Shuudin newspaper.

Please tell us about your opinions and views on Mongolia’s future?

I think that Mongolia’s economy is at a crucial stage right now. Nearly 80% of exports are provided by the mining sector. Both foreign and domestic companies and businesses are working to expand their possibilities. There is a definite need to improve infrastructure and transportation systems.

I think it would be wise to contribute major funding to infrastructure, as it will play an important role in Mongolia’s economic growth, for instance, the Tavan Tolgoi infrastructure.

Its value will significantly increase only if investors are introduced to plans and view how exactly the mining site will operate when it is completed.

I hope the Government will seriously consider this. The current work and progress of the private sector is very good. What is done in the next two years will determine how Mongolia will be in the future.

Compared to Middle Eastern countries, Mongolia has abundant oil reserves but a very low population. I have previously worked in Dubai, Abu Dhabi, and when they realized their oil reserves would soon be depleted, they lessened their dependence on oil exports and began developing other sectors.

Getting out of mining and mineral resource dependency is a very difficult task. Middle Eastern countries are attempting to improve their industrial sectors. They are attracting foreign investors through flexible tax policies and advanced infrastructure. Water and electricity supplies are already there, meaning the companies would not need initiative spending.

First of all it is important to pay attention to the education of the public, and let them understand what role mining companies like Tavan Tolgoi will play in the future; and focus on creating an economy which is not dependent on mineral resources alone.

What can Mongolia do to avoid becoming dependent on its mineral resource exports?

Mongolia has a number of advantages that Middle Eastern countries do not have. For example, the nation’s expenditure, income and deficits are open to the public. But in the Middle East, it is unknown what amount of wealth is being transferred to the Kings’ families.

In Mongolia, since these statistics are not hidden, it is possible to discuss and contemplate on how the wealth will be spent. Mongolia is in a very suitable position. Although foreign trade is currently showing deficits, but it will disappear when the economy of Mongolia becomes more stable and exports begin to increase within 2 – 5 years.

Mongolia must uphold a strategy to make sure that the future generation of Mongolians will benefit from today’s mining sector. The correct distribution of resources does not mean selling it at high prices, but making the right decision for future generations.

How is the European financial crisis affecting Mongolia?

The Mongolian economy relies on China, and China exports a large amount of goods to Europe.

The situation in Europe does not look good. It is thought that this down turn will continue for 2 – 3 years. If this continues like this there is a possibility that it will significantly affect the economy of China.

Nevertheless, the Chinese economy is estimated to grow by 7 – 8%, which is very good progress. Mongolia has a geological advantage. China imports mineral resources from Malaysia, Indonesia, and Australia. Since the quality of Mongolian mineral goods are as good as these countries, Mongolia will be very successful when the infrastructure is better developed and transportation expenses are further reduced. Additionally, to improve the quality of coal and to sell it at higher and regular market price, it is crucial that coal washing and refining plants be built.

While increasing the productivity of the mining sector, we also need to pay attention to the natural environment. This strategy should not only be carried out by mining companies but private companies as well.

Although the Chinese economy may stagger, Mongolia still has other options.

In 2008, copper made up nearly all of Mongolia’s exports, but today it is coal. So now the Mongolian economy is safe from the price instability of copper.

PM outlines three main objectives at Mongolian Economic Forum

March 7 (UB Post) Prime Minister S. Batbold said that discussions held at the 2012 Mongolian Economic Forum would play a key role in the Mongolian Government’s future decisions and strategies.

The PM stated that having more Mongolian companies listed on the Mongolian Stock Exchange. Paying careful attention to foreign investment, with the Government granting flexible taxes for new companies that create more jobs and the strong encouragement new ideas and innovation will be the three areas that receive the majority of the Government’s energy and efforts.

Both foreign and domestic delegates from businesses and organizations participated and exchanged opinions during the first day of the two-day forum on Mongolia’s rapid economic growth.

Participants focused on the correct distribution and management of wealth from mineral resources, economic and industrial diversity, social strategies, stable and balanced growth, poverty and its reduction, competitiveness, technological advancement, and innovation.

‘Mongolia’s Long-Term Development Plan and Strategy,’ was the title for the first day, with the Prime Minister. State Great Khural members N. Altankhuyag and S. Oyun, the Chairman of the Development and Innovation Committee Ch. Khashchuluun, Former Prime Minister D. Sodnom, the CEO of Oyu Tolgoi LLC Cameron McRae, and the influential political analyst B. Batbayar all in attendance.

The difficulties Mongolia is facing; notably the outdated and inefficient education system for Mongolian youth, who will become crucial human resources during this critical time of Mongolia’s economic growth, were touched on by speakers.

At the conclusion of the ‘Wealth Management and Economic Diversity,’ presentation the panelists agreed that whether a decision by the Government is made quickly or slowly, the most important matter to consider is that the decision is correct when questioned about a possible Government lag.

Mongolian PM to discuss economic issues in Japan trip

ULAN BATOR, March 6 (Xinhua) -- Prime Minister Sukhbaatar Batbold is scheduled to arrive in Tokyo on Sunday to discuss economics and other issues with Japanese leaders, the Mongolian government says.

Batbold was expected to hold talks with Prime Minister Yoshihiko Noda and meet with Yokomichi Takahiro, speaker of the House of Representatives, and Kenji Hirata, president of the Senate.

Batbold and Noda were to hold talks on the expansion of bilateral cooperation, especially in economics, and an easing of travel restrictions.